When it comes time for annual enrollment, you face a lot of choices: Which health plan should I choose? What benefits matter most? And, inevitably, should I contribute to a Flexible Spending Account (FSA)?

But many employers now invite another question: Which type of Flexible Spending Account do I need? As millions of employees demand better benefits and perks, employers are offering several FSA options, including Limited Purpose FSAs (LPFSAs) and Dependent Care FSAs (DCFSAs).

Flexible Spending Accounts are ultimately very simple to use, but there are differences you should be aware of as you make your benefits elections.

This article compares three FSA account types to reveal surprising differences between healthcare FSAs, Limited Purpose FSAs, and Dependent Care FSAs.

How does an FSA work?

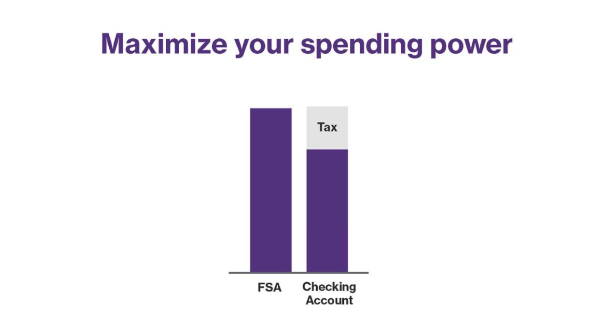

First let’s talk about what these three accounts have in common. Any Flexible Spending Account lets you make pre-tax payroll contributions to pay for eligible expenses.

In other words, FSAs help you unlock significant tax savings and boost your potential spending power. Since the money you contribute and spend is not taxed, you have more money to put toward eligible expenses.1

Some accounts come with a dedicated debit card2 to let you pay directly out of your Flexible Spending Account. However, reimbursement is easy too. Simply pay out of pocket with your personal payment method, then upload and submit a receipt for reimbursement. Usually, money will transfer from your FSA to your checking account within a few days.

What can I pay for?

All FSA types let you make pre-tax payroll contributions to pay for eligible expenses. But what counts as an eligible expense differs between the account types. Here is a summary.

- Healthcare FSAs let you pay for all eligible medical expenses, including dental and vision expenses, as well as over-the-counter medications.

- Limited Purpose FSAs restrict eligible expenses to dental and vision eligible medical expenses exclusively.

- Dependent Care FSAs restrict eligible expenses to dependent care expenses exclusively. A qualifying ‘dependent’ may be a child under age 13, a disabled spouse, or an older parent in eldercare.

The table below illustrates common eligible expenses. These lists are by no means exhaustive.

Healthcare FSA | Limited Purpose FSA | Dependent Care FSA |

|---|---|---|

|

|

|

Who is eligible?

Healthcare FSAs, LPFSAs, and DCFSAs are all employer-sponsored accounts. This means you can only enroll in these accounts through your employer. If your employer doesn’t offer one of these FSAs, then you won’t be able to take advantage of potential tax savings.

In the case of healthcare FSAs, your spouse can elect a Health FSA as well, provided their employer offers a Health FSA benefit. This empowers families to essentially double the maximum contribution limit. The same is true for a Limited Purpose Flexible Spending Account also.

Dependent Care FSAs have slightly different rules. In the event of divorce, only the parent with custody can use DCFSA funds to pay for dependent care. Per IRS rules, where custody is split, DCFSA eligibility is determined according to the household at which the dependent spends the greater number of nights during the calendar year. If custody is evenly split there, too, then eligibility is prioritized according to whichever parent earns the highest income.

Learn more in our article: Five DCFSA rules you need to know.

Who is covered?

Even if your spouse doesn’t open their own Flexible Spending Account, you can use the money in your FSA to pay for their eligible medical expenses. You’re allowed to spend FSA dollars on your eligible dependents as well (see everything you can buy at the FSA Store).3

The same is true for Limited Purpose FSAs and mostly true Dependent Care FSAs. The only difference with DCFSA is that you cannot pay for your spouse unless they qualify under the DCFSA as an eligible dependent.

Which accounts are HSA-compatible?

Millions of Americans choose high-deductible health plans (HDHP). In general, these health plans offer comparatively lower premiums and more flexibility.

HDHPs also offer another important perk: Eligibility to make contributions to a Health Savings Account (HSA). That is, you can only make HSA contributions if you’re enrolled in an HSA-qualified health plan.

Generally, a healthcare FSA is compatible with most major health plan types. But if you contribute to a healthcare FSA, then you are ineligible to contribute to a Health Savings Account.

You can, however, use an LPFSA and a DCFSA with an HSA. Pairing an LPFSA with an HSA is a great way to maximize the value of both accounts. Simply use the LPFSA to pay for dental and vision expenses, then save your HSA for long-term future healthcare costs.

When are funds available?

During annual enrollment season, you’ll need to elect an FSA as well as your annual contribution amount. Let’s say you elect to contribute $1,500 for the plan year. Your employer will deduct $1,500—usually in equal increments—from your paychecks over the course of the year.

So, if you receive 24 paychecks in a year, you can expect $62.50 deducted from each.

Here’s the cool thing. The entire $1,500 will be available on the first day of the new plan year. There’s no need to wait for your payroll contributions to accrue a balance. That means you essentially get an advance from your employer to help cover the cost of eligible medical expenses. And in practice it means you don’t have to wait until the end of the year to pay an eligible large medical expense.

The same rules apply to Limited Purpose FSAs as well. You get your full annual contribution amount on the first day of the plan year.

Dependent Care FSAs, however, work differently. Your balance only accrues as you make contributions. In most cases this isn’t usually a problem since members typically pay their daycare and dependent care providers on a recurring basis anyway.

You can always view the latest IRS contribution limits at this page.4

Wrapping up

We covered a lot in this article. Here’s everything you need to know in a quick summary.

Healthcare | Limited Purpose | Dependent Care | |

|---|---|---|---|

Eligible expenses | Eligible medical expenses, including dental and vision | Eligible dental and vision expenses only | Eligible dependent care expenses only |

Requires employer to offer account | Yes | Yes | Yes |

Who is eligible to enroll? | Either (or both) spouse may open a healthcare FSA | Either (or both) spouse may open an LPFSA | Either (or both) spouse may open a DCFSA |

On whom can you spend the funds | Yourself, your spouse, your eligible dependents | Yourself, your spouse, your eligible dependents | Eligible dependents |

HSA compatible? | No | Yes | Yes |

Fund availability | Full annual balance available on day one | Full annual balance on day one | Funds are available only as you make contributions |

Have questions? Visit our Help Center.

Ready to shop? Visit the FSA Store.3

HealthEquity does not provide legal, tax or financial advice. Always consult a professional when making life-changing decisions.

1FSAs are never taxed at a federal income tax level when used appropriately for qualified medical expenses. Also, most states recognize FSA funds as tax deductible with very few exceptions. Please consult a tax advisor regarding your state’s specific rules.

2This card is issued by the Bancorp Bank, N.A. pursuant to a license from Visa U.S.A., Inc. Your card can be used everywhere Visa debit cards are accepted for qualified expenses. This card cannot be used at ATMs and you cannot get cash back, and cannot be used at gas stations, restaurants, or other establishments not health-related. For card terms and conditions, see the Cardholder Agreement that is provided with the card.

3HealthEquity and the FSA Store are separate companies and are not responsible for each other’s policies or services. When you make a purchase through the FSA Store from a link on a HealthEquity site, we may earn a referral commission.

4For the latest contribution limits please visit: Healthequity.com/learn.